19 Feb When Interest Rates Rise, Housing Delivery Risk Changes

A 0.25 percentage point interest rate rise does more than lift mortgage repayment. It shifts the risk profile of housing delivery across Australia, changing what households can afford, developers can build, and local governments can realistically expect to see delivered.

The Reserve Bank of Australia’s (RBA) February 2026 decision to increase the cash rate to 3.85% marks a return to a tightening cycle, with its first rate rise in over two years. For many households, the impact is clear, with typical mortgage payments rising by around $100 per month.

However, the larger story is less visible. Rising rates don’t simply cool demand in the present. They reshape how housing demand, supply and pressure interact, often in ways that are not immediately visible in headline data. Higher rates alter the pipeline that turns current approvals into future homes, exposing the fragility of Australia’s housing delivery system.

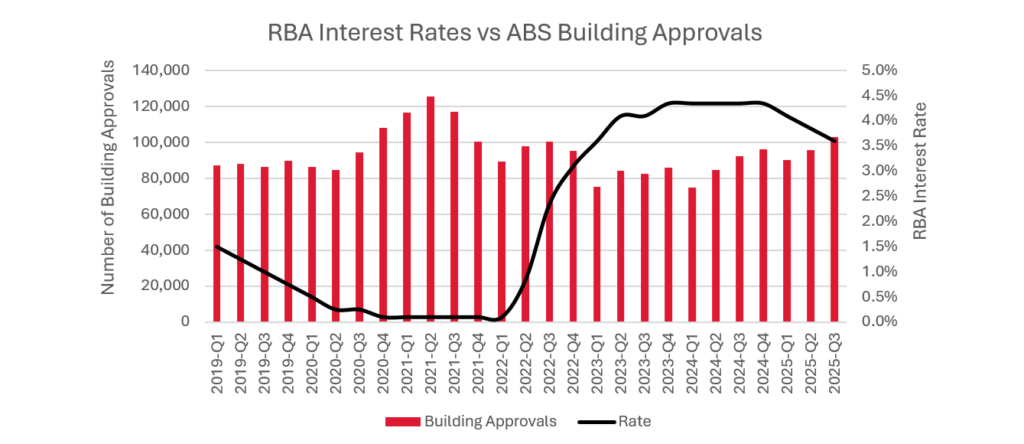

The following chart shows an inverse relationship between the RBA cash rate and ABS building approvals, but importantly, the impact is not immediate. Approvals begin to soften, generally 2-4 quarters after sustained rate increases. Building approvals are a leading indicator of future dwelling supply. If they slow materially, the supply shortfall emerges 12-24 months later. In summary, when interest rates rise, the following occurs: Rates up → Confidence shifts → Feasibility tightens → Approvals decline (with delay).

REMPLAN has previously examined how RBA rate cuts could accelerate housing demand. The analysis highlighted that interest rates change behaviour then housing outcomes. Lower rates were expected to improve borrowing capacity, lift confidence, and reaccelerate demand, particularly in constrained markets.

Why This Matters For Housing

As of early 2026, inflation remained high, leading to the rate hike, with projections indicating inflation will stay above target for some time. Increasing interest rates place additional pressure on mortgage holders and slow housing activity, particularly in areas where property values and rents are already high.

The impact of interest rate changes move through the housing system in stages.

First, borrowing capacity tightens. This can reduce buyer demand, particularly among first home buyers. In some markets, price growth softens. In others, constrained supply and strong population growth keep prices elevated despite higher rates.

Second, development feasibility weakens at the margins. Higher financing costs add to existing pressures from construction costs, labour shortages, and infrastructure contributions. Projects that were previously viable under lower rates can become marginal. Some are delayed. Others remain approved but do not proceed.

This creates an approval illusion that many Councils are now experiencing. Approval numbers may remain steady, yet commencements and completions often slow down or flatten. In theory, supply appears healthy. On the ground, commencements and delivery slows.

While such demand-moderating outcomes are not unexpected and are central to the RBA’s core mandate of containing inflation within the target range, they can run counter to efforts to address other challenges that Australia faces. Housing affordability and accessibility are a case in point.

To truly understand what’s happening in housing markets, and who is being affected, general commentary isn’t enough. Some areas with strong employment and income growth may weather rate rises better than those with weaker local economic fundamentals. Localised, detailed data is critical.

What This Means for Councils and Practitioners

Rising rates create three practical risks for Councils:

- Delivery risk behind housing targets: Meeting approval targets does not guarantee delivery. As feasibility tightens, the gap between approvals and completions widens. Monitoring pipeline risk is now essential.

- Concentrated affordability pressure: Higher repayments and rents impact suburbs and income groups unevenly. Without local evidence, emerging housing stress and service demand are easy to miss.

- Workforce and service impacts: Rental affordability increasingly affects essential workers. In tight markets, housing constraints directly limit workforce attraction and service delivery

Interest rate movements are therefore not simply financial events. They impact land supply conversions, dwelling commencements, liveability, and regional competitiveness.

Illuminating the Real Story with Local Data: Monitoring the Impact of Interest Rate Rises

Housing affordability and stress vary across regions, tenure types, and income brackets. Behind every broad headline about interest rates lies a local story of affordability, demand, and community impact. The REMPLAN suite of housing data tools helps reveal these patterns.

Track affordability in changing market conditions

A rate rise tightens borrowing power, but local conditions, including supply constraints or strong rental demand, might offset or amplify its effects. Localised affordability metrics highlight where housing costs already exceed the 30 per cent income benchmark and reveal whether affordability is worsening or improving in specific areas.

Reveal uneven impacts across your community

Higher repayments may squeeze some households more than others. First-home buyers and low-income renters are often the most vulnerable when rates rise and rents continue to climb. Locality level insights can pinpoint where support is most needed within council areas.

Monitor housing stress over time

Longer-term trends in mortgage and rental stress data show whether short-term moves in interest rates translate into persistent affordability issues in your region. Housing stress profiles reveal which households are most stretched by repayments and rents.

Connect market activity with demographic shifts

Interest rates influence buyer demand, rental market dynamics, and household movement patterns. Combining housing market data with demographic trends helps assess whether demand reflects real local needs or speculative pressures. Demographic overlays show how population growth, workforce participation, and household formation intersect with market trends.

Monitor Your Local Housing Supply, Affordability and Stress with REMPLAN Housing

REMPLAN Housing profiles provide clear, location-specific insights that empower councils, planners, policymakers, and community organisations, to understand current conditions and monitor changes over time.

Visit REMPLAN Housing for more information about how localised housing data can support clearer planning, stronger evidence, and more confident decisions in a higher interest rate environment.

For your chosen region, REMPLAN Housing profiles deliver:

- Mortgage and rental stress by income level

- Housing affordability measures

- Demographic insights including population trends and workforce data

- Market trends showing median house, unit, and land prices over time

- Dwelling demand forecasts alongside building approvals data

The latest RBA rate change is more than a macroeconomic headline; it’s a policy shift with real consequences for local housing markets. In a shifting interest rate environment, REMPLAN Housing helps councils turn complex market signals into clear, actionable local insights.

Contact the REMPLAN team to request a demo or start your REMPLAN journey today.

No Comments